SMM January 15 News:

The calendar year 2024 has ended. Domestic demand for galvanized sheet remained weak, but exports grew strongly, with mixed changes in end-use orders. Additionally, cold-rolled prices in H1 mostly declined until a rebound around the National Day holiday, which also led to weaker MoM galvanized sheet finished product prices. The "rush to buy amid continuous price rise and hold back amid price downturn" sentiment also disrupted end-use purchasing sentiment for galvanized sheets. Under the influence of multiple factors, how did domestic galvanized sheet mills perform in 2024? We analyze this from the perspective of end-use demand.

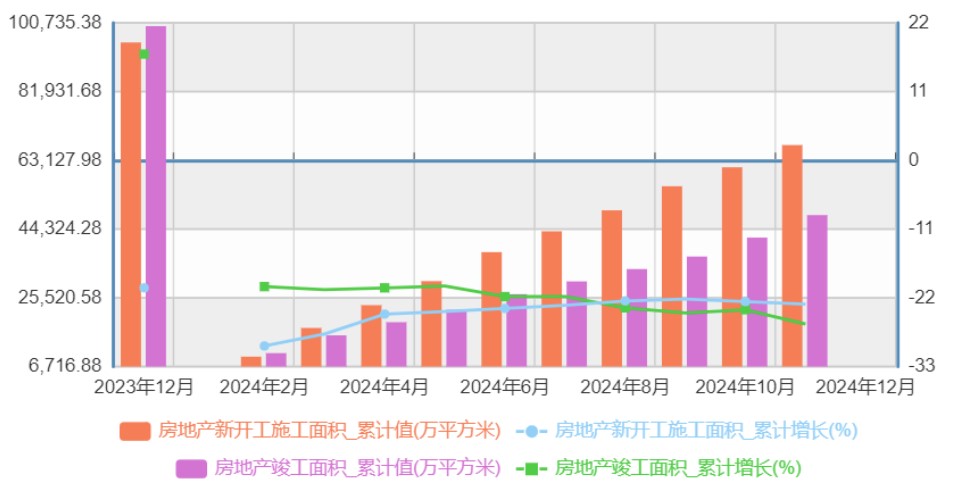

Construction Sector. In 2024, China's real estate market saw frequent favorable policies, ranging from lowering mortgage rates in H1 to the "three arrows" policy in H2, continuously boosting market expectations. However, specific data shows that from January to November 2024, national real estate development investment totaled 9,363.4 billion yuan, down 10.4% YoY. The cumulative completed area of real estate was 481.51 million m², down 23% YoY, and the cumulative new construction area was 673.08 million m², also down 23% YoY. As a major downstream consumption sector for zinc, the poor performance of construction-related project data continued to drag down domestic galvanized sheet mill orders in 2024.

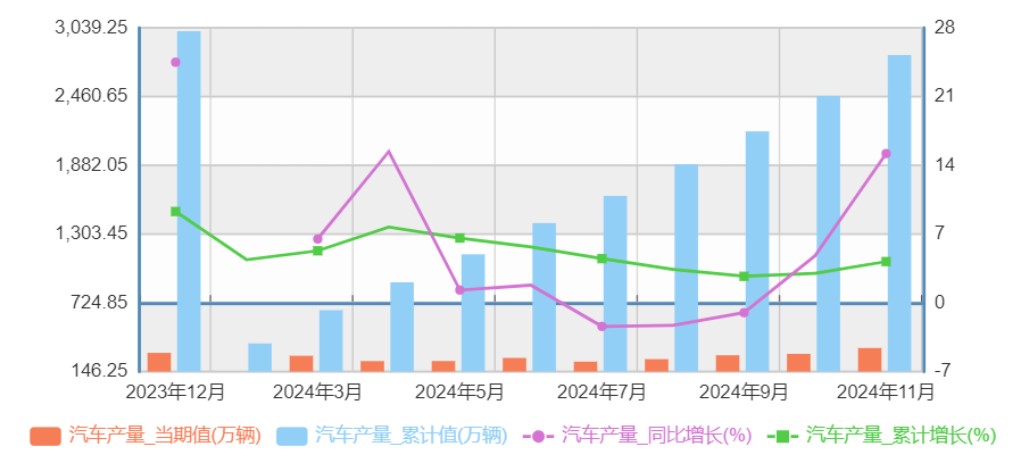

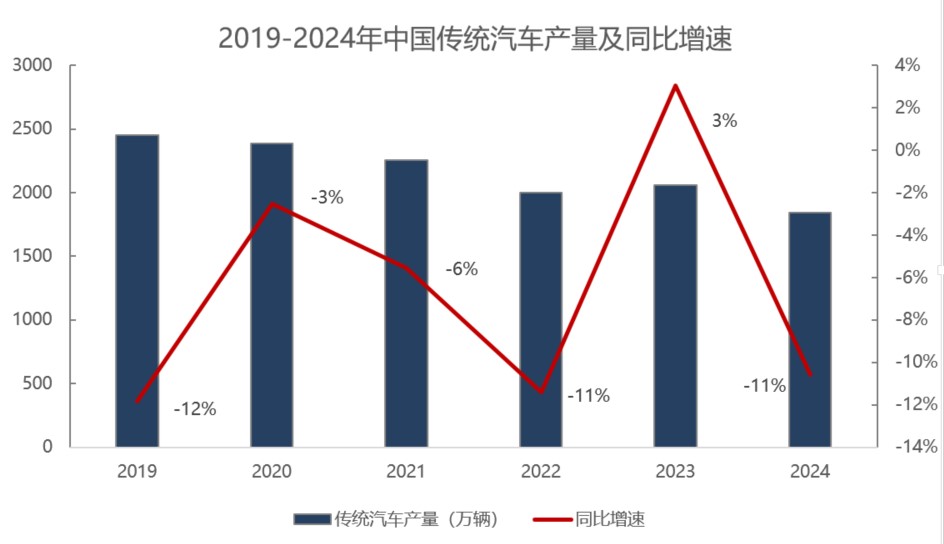

Automotive Sector. In 2024, China's automobile production reached 31.282 million units, up 3.70% YoY, and sales reached 31.436 million units, up 4.50% YoY, showing strong performance. However, it is worth noting that the market share of NEVs increased from about 30% in 2023 to 40%, while the production and sales of traditional fuel vehicles declined by 10% YoY. Since galvanized sheets are mainly used in certain traditional mid-to-high-end fuel car models, the demand for galvanized sheets in the automotive industry in 2024 saw limited growth.

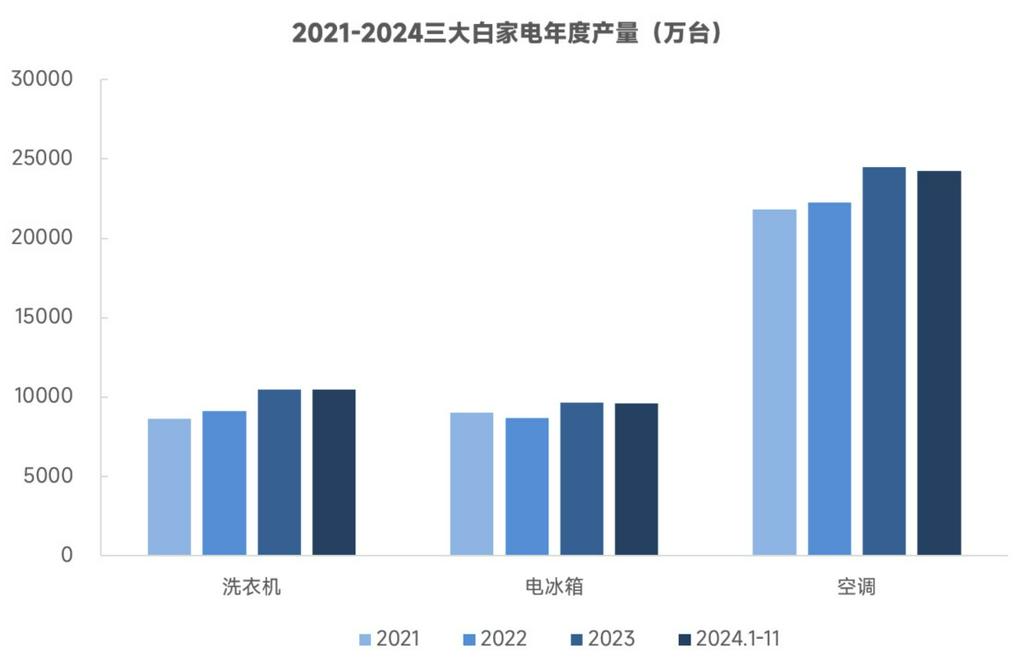

Home Appliance Sector. On the domestic demand side, policies such as "trade-in" were introduced in H1 2024, with local governments responding by launching related replacement subsidies. With the continued implementation of these policies, domestic home appliance-related orders improved in H2. Additionally, China's home appliance exports performed strongly in 2024. Driven by exports and policy support, the production of white goods from January to November 2024 was on par with 2023. Including December data, it is expected that galvanized sheet orders in the home appliance sector in 2024 will increase compared to 2023.

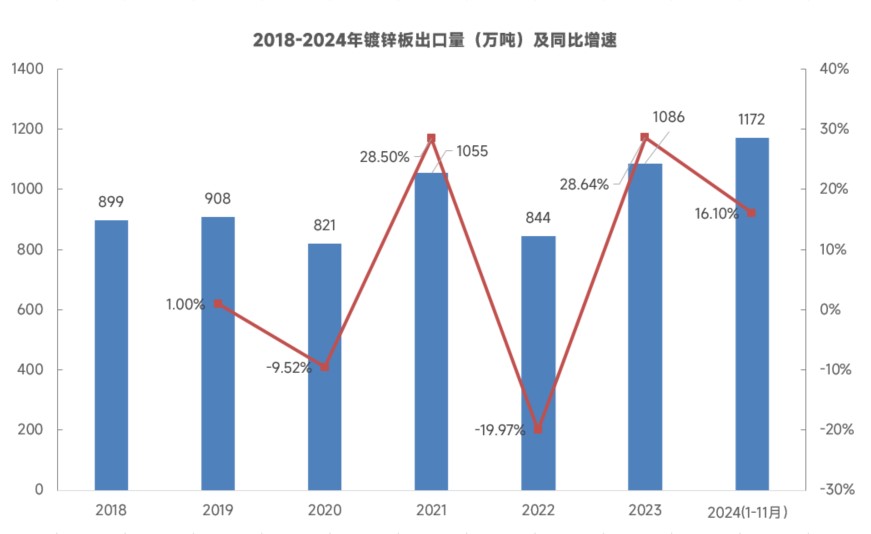

Export Sector. Since April this year, countries or organizations such as Colombia, Ukraine, Pakistan, Brazil, and the Eurasian Economic Commission have successively launched anti-dumping investigations on Chinese galvanized coils. However, data shows that from January to November 2024, China's cumulative exports of galvanized sheets reached 11.716 million mt, up 16.1% YoY. The anti-dumping investigations have not yet caused significant impacts. Moreover, the noticeable decline in galvanized sheet prices compared to 2023 provided a price advantage, contributing to the strong export performance of Chinese galvanized sheets in 2024.

Outlook for the Market. Currently, relevant construction data has not shown significant improvement. The automotive sector is expected to see a continued increase in the share of NEVs. Considering potential disruptions in the global foreign trade market in 2025, it remains uncertain whether the strong performance of home appliances and galvanized sheet exports can be sustained. With limited growth in demand across end-use sectors, China's galvanized sheet development this year is expected to face certain challenges.

For SMM Lead and Zinc Industry Data Package, please contact: Penghui Tang

Phone: 15008461791